Topic 842 will be replacing FAS 13/Topic 840. It's the FASB's equivalent of IFRS 16 and their own new standards to help realign lease accountancy and reporting with modern day leasing habits. The changes are broadly similar to IFRS 16, but the biggest headline difference is that the implementation deadline and options are different. These are:

If you follow FASB standardised practice, then here is a useful download to help you understand Topic 842 further.

IFRS 16 states a lease as: 'a contract, or part of a contact, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.' A lease exists when a customer controls the right to use an identified item, which is when the customer:

It's expected that agreements that were formerly considered leases under IAS 17 may no longer meet the IFRS 16 specification and vice versa.

Now that all leases will be accounted for "on balance sheet", operating leases will, in effect, cease to exist. At least, that is to say, lease agreements will no longer be classified as an operating lease as they currently are under IAS 17. Instead of being based on risk and reward, the classification of a lease will focus on control of the right of use of an asset; namely the difference between a lease and a service.

Although in principle, the definition of a lease in IFRS 16 is similar to under IAS 17, there is more detail regarding the classification of a lease.

IFRS 16 contains new guidelines towards the definition of a lease that differs from the current definition features in IAS 17 and IFRIC 4. This is to provide further clarity between the classification of a lease agreement and other agreements, such as a service contract.

A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. A contract can qualify as a lease or as containing a lease if:

IFRS 16 only affects leases; if an agreement does not contain a lease, then there is no need to recognise the arising 'assets' and liabilities on balance sheet. A different accounting standard would apply instead.

Here's a handy webcast on the definition of a lease from IFRS.org (link opens in new window).

When it comes to being able to truly understand what constitutes a lease under IFRS 16 and ensure you don't accidentally breach compliance, you can speak to a leasing expert or use this free explanatory guide. The e-Paper aims to provide a detailed overview of the new definition of a lease, its associated implications and provides practical advice on how businesses are able to navigate the changes of IFRS 16.

Increasing transparency and allowing easier comparability is the aim of the new standards, but in achieving this, there are new challenges that businesses are facing. Primarily, a full valuation of your lease portfolio needs to take place, and here we highlight some of the challenges you're now up against:

For further explanations on this topic, PKF Littlejohn LLP has produced a thorough look at what IFRS 16 means for you and your clients. Also, on a related theme, you might find these posts useful too: How To Make The Lease Accounting Data Collation Process A Success, How Will IFRS 16 Impact Business KPIs and Financial Performance Metrics? and Which Transition Method Should I Use? The Pros And Cons Of Each Method.

Organisation, proper prior planning and structured communication are the three core elements to achieving lease accounting compliance. The larger your lease portfolio, the larger the task at hand and the earlier preparatory work should begin. Or, rather, should have begun. With the implementation deadline of 1st January 2019 creeping ever closer and your business possibly benefiting from early adoption, work if not begun now starts with getting organised.

Compliance with the new standards can be achieved by tackling the process in seven distinct steps.

Wondering how to get buy-in from your accounts department? Read this.

If those 7 steps raised a few more questions or made you think of a few potential exposure points when achieving compliance, take a look at this deep dive document. The 7 Steps to Lease Accounting Compliance eBook is a thorough and easy to understand, designed to give you a full overview of the standards and a practical explanation of the implications. It also outlines the seven steps to compliance, above, in full detail, with extra guidance on each step.

It's a great resource for furthering your own understanding and helping to illustrate to colleagues or bosses why leasing changes do, in fact, impact your business.

They already have. And this statement is not as flippant as it first sounds because you've already searched out explanations on the topic, but because it's typical that preparation for compliance can take up to two years.

In the first instance, the magnitude and number of changes which are required in order to get ready for IFRS 16 mean that it simply takes time and resource to prepare. Besides the whole host of knock-on impacts from the changes, such as the effect that IFRS 16 will have on key financial metrics, the biggest single change is that operating leases will, as a result of the new standards, effectively cease to exist as a separate category for accounting purposes.

These changes mean that all leases will now be represented on balance sheet. To illustrate, an estimated US$2.8 Trillion is expected to drop onto balance sheet reports and this change must impact profit and loss accordingly.

Furthermore, the definition of what actually constitutes a lease and what constitutes a service agreement is changing, and vice versa. What this means to you is that your company will need to gather and assess all the related agreements and associated paperwork in order to begin ensuring compliance is achieved in time for the deadline.

And the second broadly-complicating reason for the early need to prepare for IFRS 16 is that there are possible exemptions, early adoption and required retrospective reports that need consideration.

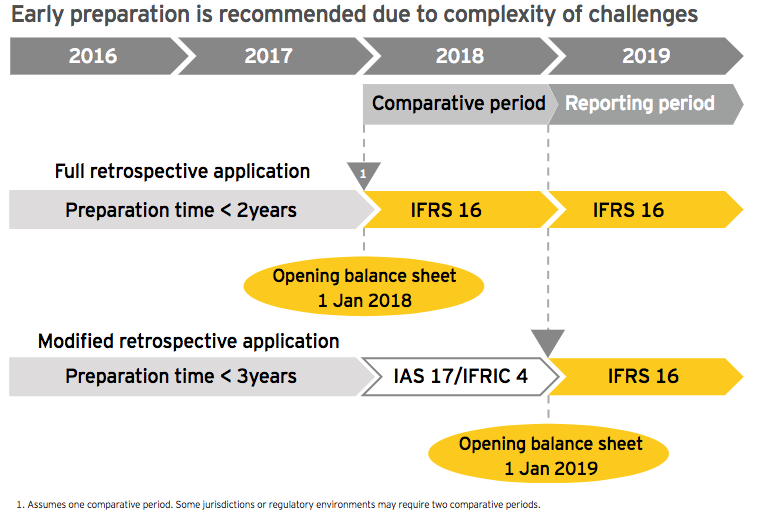

Ernst & Young advise in their ePaper on the topic, Leases - A summary of IFRS 16 and its effects, that with reporting for IFRS 16 beginning on 1st January 2019 at the latest, assuming a modified retrospective application is employed, the latest preparation should begin is during 2016. The level of complexity in understanding the new standards, gathering all the data required in order to fully assess the situation and then creating the proper reports are just three headline factors which make compliance such a long process.

Extract from Ernst & Young's paper on IFRS 16.

Compliance is no quick fix. It's complex and also unlikely that the team dedicated to achieving compliance will have the task as their sole focus. At best, it's going to detract from their ordinary responsibilities and at worst it will have direct financial implications if left non-compliant.

These factors hint at some of the secondary impacts of IFRS 16. Read about the subject further here and on the rest of our blog and subscribe for updates.

The impact of the new standard will differ on a company by company and industry by industry basis, dependent upon factors such as the size of an entity’s leasing portfolio, internal processes and reporting structures or the demands of the industry.

Some industries will be more likely to be impacted by lease accounting changes. As mentioned, the aviation industry is an example which grabs the headlines due to the unlikely nature of Acme Passenger Airways' passenger planes not being shown on balance sheets as an operating cost, but other sectors are facing a bigger task.

The retail industry and courier or haulier companies, for example, are two which rely heavily on leased property and assets in order to stay agile and keep overheads low, whilst accessing the most current equipment. Leasing is vital to how certain sectors function.

We have already produced a range of resources to help particular industries in particular. Just head to the page from the list below which applies to your business' industry or sector.